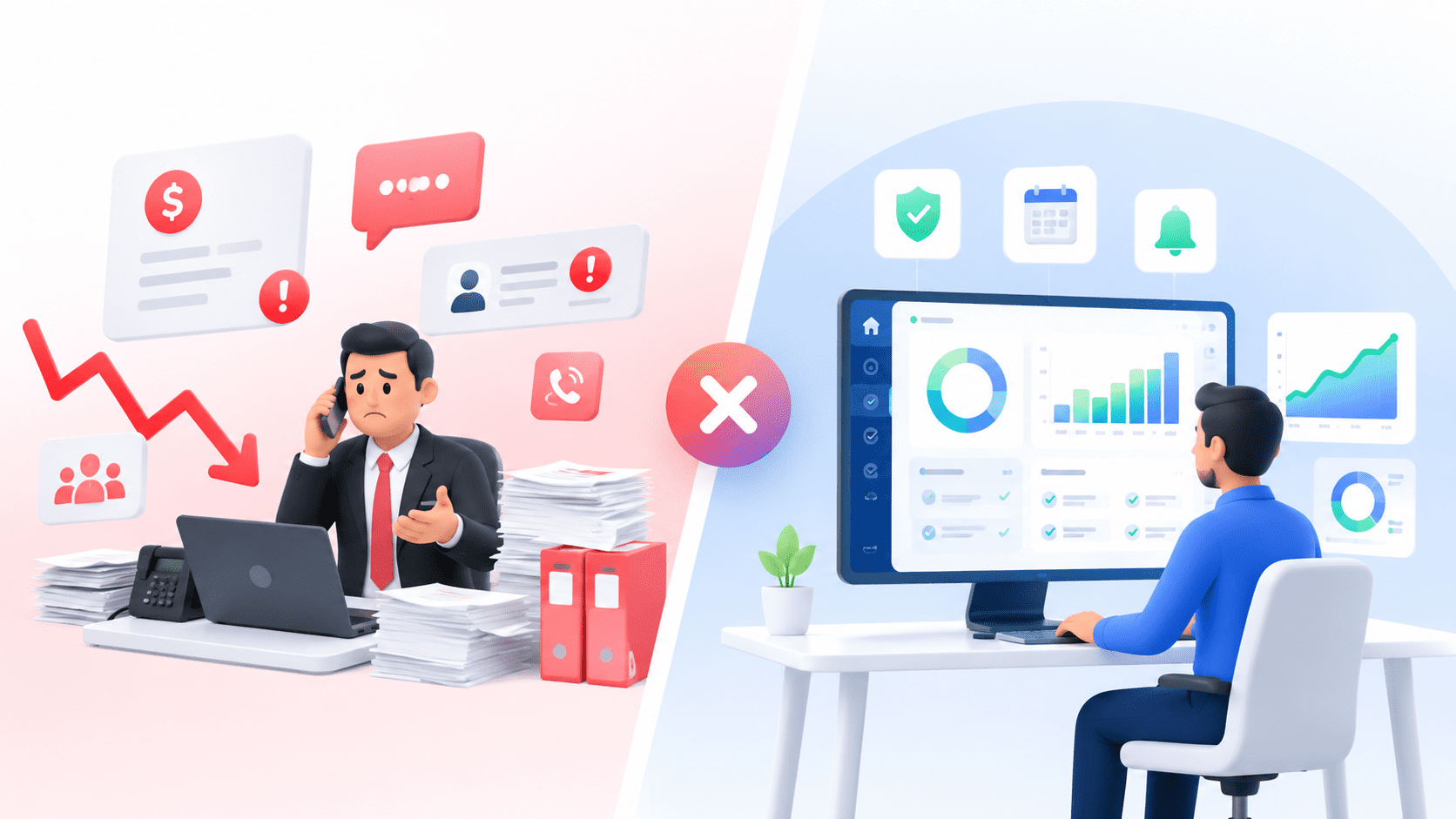

When cash flow tightens, many businesses instinctively turn to collection agencies to recover overdue payments—but the reality is that a collection agencies are not the best for collections in today’s fast-moving, customer-first environment.

What seems like a quick fix often results in higher costs, slower recovery, and a complete loss of control over customer relationships.

Table of Contents

Why Collection Agency Are Not The Best for Collections in Modern Finance?

For decades, collection agencies have been the default option for recovering unpaid invoices. But modern finance teams are rethinking this approach.

With rising customer expectations and the need for predictable cash flow, it’s becoming increasingly clear that a collection agency is not best for collections when compared to proactive, technology-driven strategies.

The Real Cost: Why Collection Agency are not Best for Collections

High commissions eat into your revenue

Collection agencies typically charge between 20% to 50% of the recovered amount.

That means:

- Recover ₹10 lakhs → lose ₹2–5 lakhs instantly

- And this often happens after months of delay

Instead of improving cash flow, you’re effectively discounting your own revenue—one of the biggest reasons why a collection agency not best for collections for growing businesses.

You Lose Customer Relationships (Sometimes Forever)

Collections become aggressive—and impersonal

When collections are outsourced:

- You lose control over how customers are approached

- Communication often becomes aggressive or transactional

- Trust breaks down quickly

In B2B, this can mean losing not just a payment—but an entire account.

That’s another reason why a collection agency not best for collections when long-term relationships matter.

It’s Already Too Late When Collection Agencies Step In

Agencies work on aged debt—not active receivables

Most companies send accounts to collection agencies after 60–90 days of non-payment.

By then:

- Recovery rates have already dropped

- Customers are less responsive

- Disputes are harder to resolve

At this stage, you’re not managing collections—you’re trying to recover what’s already slipping away.

Collection Agency Not Best for Collections Because It Lacks Strategy

They treat every account the same

Collection agencies are designed for volume, not nuance.

Their approach typically includes:

- Standard follow-up scripts

- Repetitive calls and emails

- Generic workflows

But real-world collections involve:

- Complex invoices

- Payment disputes

- Internal approval delays

Without context, recovery becomes inefficient—reinforcing why a collection agency not best for collections in modern finance operations.

No Guarantees, Only Hope

Even after investing time and money:

- There’s no guarantee of recovery

- Some debts remain uncollected

- Legal escalation increases costs further

You’re essentially outsourcing uncertainty, not solving the root problem.

The Real Problem: Collections Start Too Late

Here’s what most businesses overlook:

Collections problems don’t start at 90 days—they start on Day 1.

Late payments are often caused by:

- Delayed or unclear invoicing

- Lack of consistent follow-ups

- Poor visibility into receivables

- Disconnected finance and sales processes

By the time a collection agency is involved, the issue has already escalated.

What Works Better Than Collection Agency Not Best for Collections?

Proactive, tech-driven collections

Modern finance teams are moving toward proactive receivables management instead of reactive recovery.

This includes:

✔ Automated reminders before due dates

✔ Real-time payment tracking

✔ Customer risk scoring

✔ Smart escalation workflows

✔ Centralized AR visibility

The result:

- Faster payments

- Lower bad debt

- Stronger customer relationships

Conclusion

Collection agencies are not the best for collections if your goal is predictable cash flow and long-term growth.

While they may help in extreme situations, they fall short for everyday collections because:

- They act too late

- They cost too much

- They lack strategic insight

The future of collections isn’t about chasing payments harder—it’s about managing them smarter from the start.

About FinFloh

FinFloh helps finance teams take control of their collections before they become problems.

With FinFloh, you can:

- Automate collections workflows

- Gain real-time visibility into receivables

- Use intelligent insights to prioritize accounts

- Improve cash flow predictability

Instead of reacting to delays, you stay ahead of them.

Still relying on outdated collection methods?

Book a demo with FinFloh and discover how to reduce DSO, improve collections efficiency, and unlock faster cash flow.