Category: Collections

-

How Payment Behavior Predicts Default Before It Happens

Most businesses recognize customer default risk only after invoices become severely overdue, collections efforts fail, or legal escalation begins. By that point, the financial impact is already visible in cash flow, bad debt exposure, and working capital pressure. But customer defaults rarely happen suddenly. In most cases, customers exhibit warning…

-

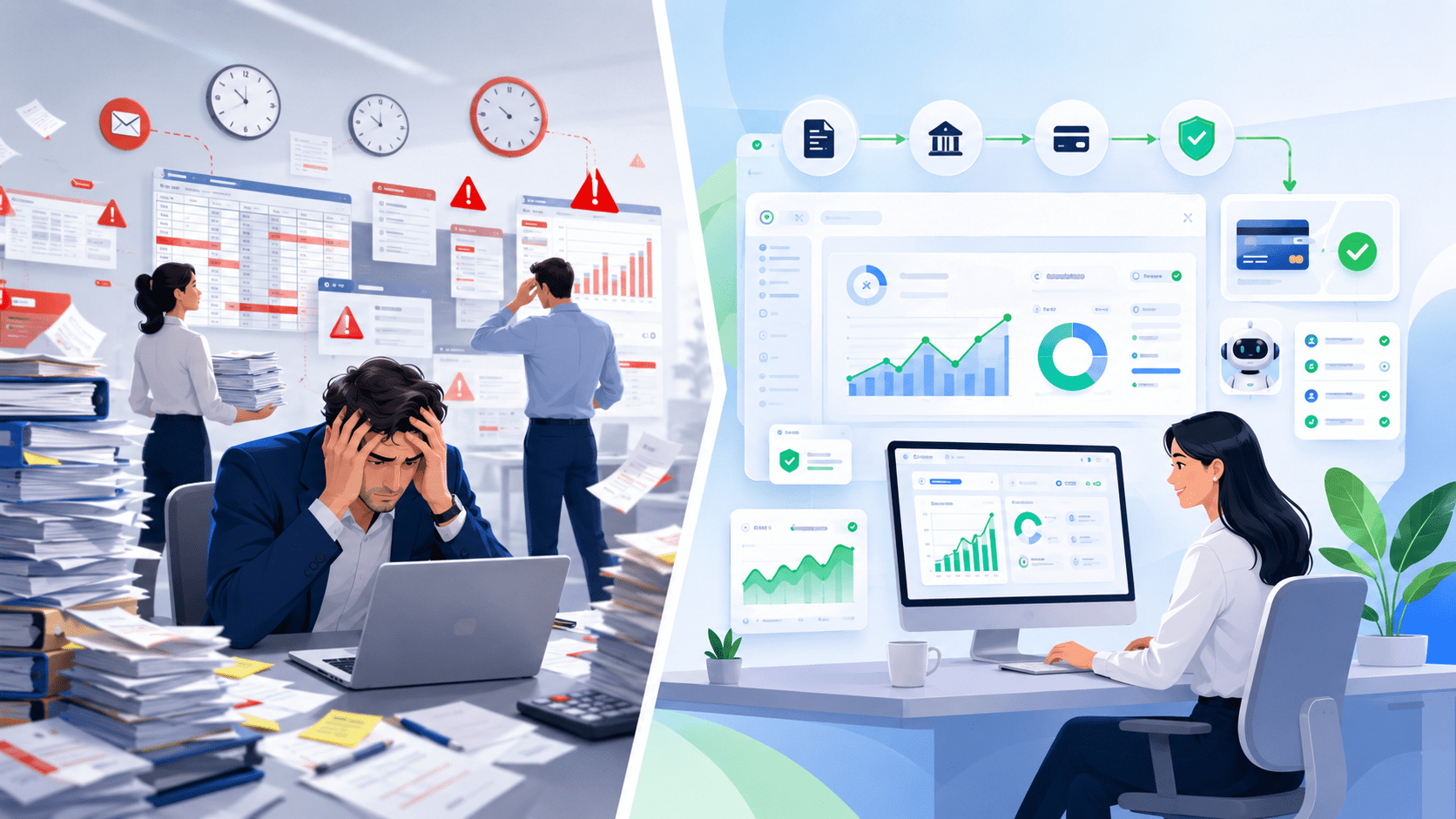

5 Risks Accounts Receivable Teams Face Today

Managing receivables is no longer just about sending invoices and waiting for payments. Today, finance teams face multiple accounts receivable risks that directly impact cash flow, customer relationships, and business growth. From delayed payments to fraud and inaccurate reporting, even a small inefficiency in accounts receivable can create major financial…

-

Promise-to-Pay Data: The Most Underutilized Treasury Signal

Treasury teams rely heavily on forecasts, liquidity models, historical payment trends, and banking data to predict cash flow. Yet one of the most valuable indicators of short-term cash movement is often overlooked entirely: Promise-to-Pay (PTP) data. Every day, customers communicate expected payment dates to collections teams through emails, calls, portals,…

-

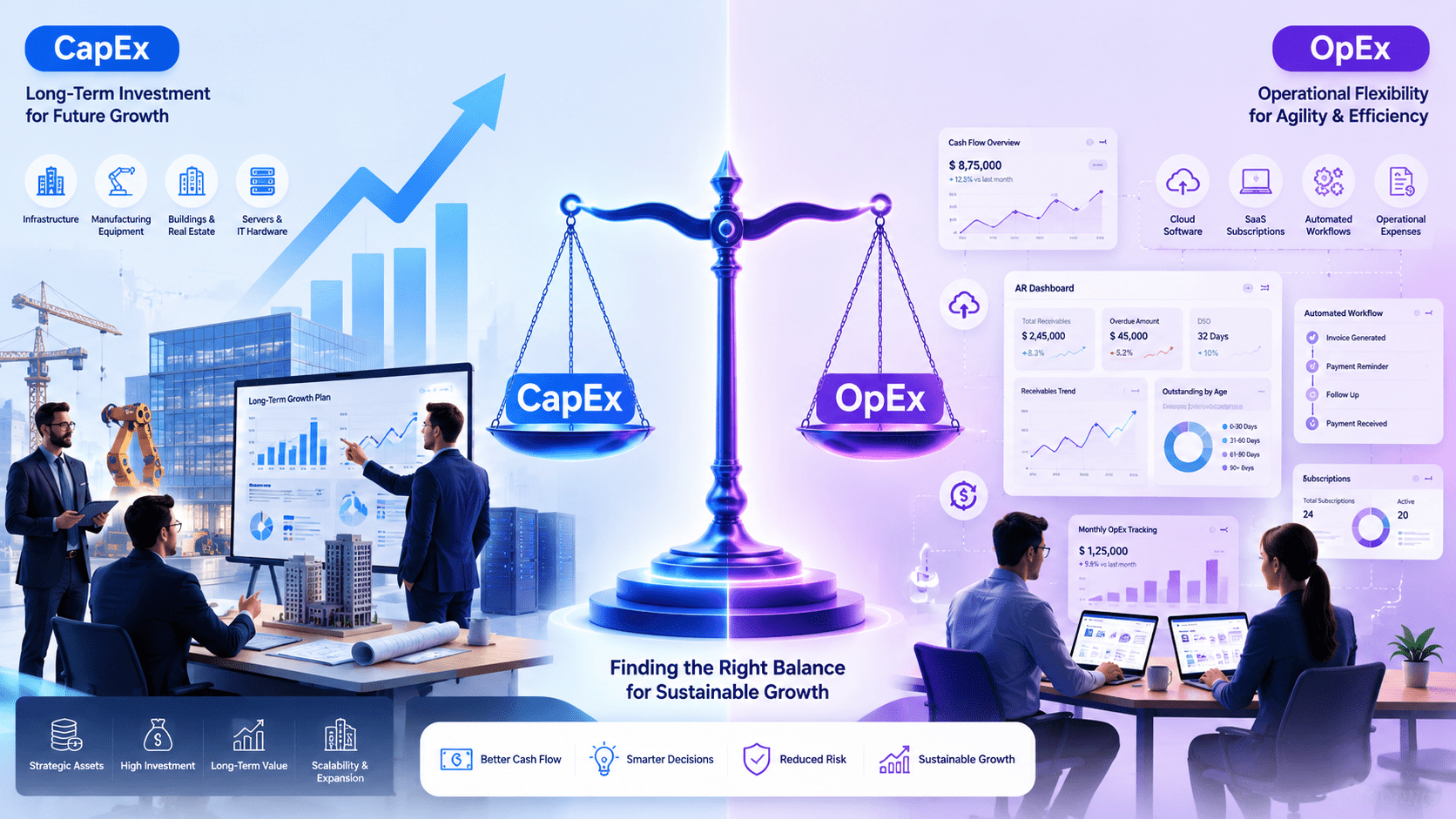

CapEx vs OpEx: Finding the Right Balance for Business Growth

Every growing business eventually faces the same financial question:Should we invest heavily in long-term assets or keep operations flexible with ongoing expenses? Finding the right balance between CapEx and OpEx is critical for maintaining healthy cash flow, improving operational efficiency, and scaling sustainably. While both play an important role in…

-

B2B Payment Modes: A Complete Guide for Modern Businesses

Efficient payment processes are critical for every business. In B2B transactions, payment methods directly impact cash flow, customer relationships, operational efficiency, and working capital management. Unlike consumer payments, B2B payments often involve higher transaction values, credit terms, invoice-based billing, and multiple approval workflows. As businesses become more digital, organizations are…

-

Why CFOs Are Prioritizing B2B Payment Automation

Finance teams today are under more pressure than ever. CFOs are expected to improve cash flow, reduce operational costs, accelerate collections, and deliver real-time financial visibility — all while managing leaner teams and rising customer expectations. That’s exactly why B2B payment automation has become a top priority for modern finance…

-

What Is Payment Tokenization and Why Businesses Need It?

Digital payments have become the backbone of modern business. But as online transactions grow, so do concerns around fraud, data breaches, and payment security. That’s where Payment Tokenization comes in. From ecommerce brands to SaaS companies and B2B finance teams, businesses today rely on payment tokenization to protect sensitive payment…

-

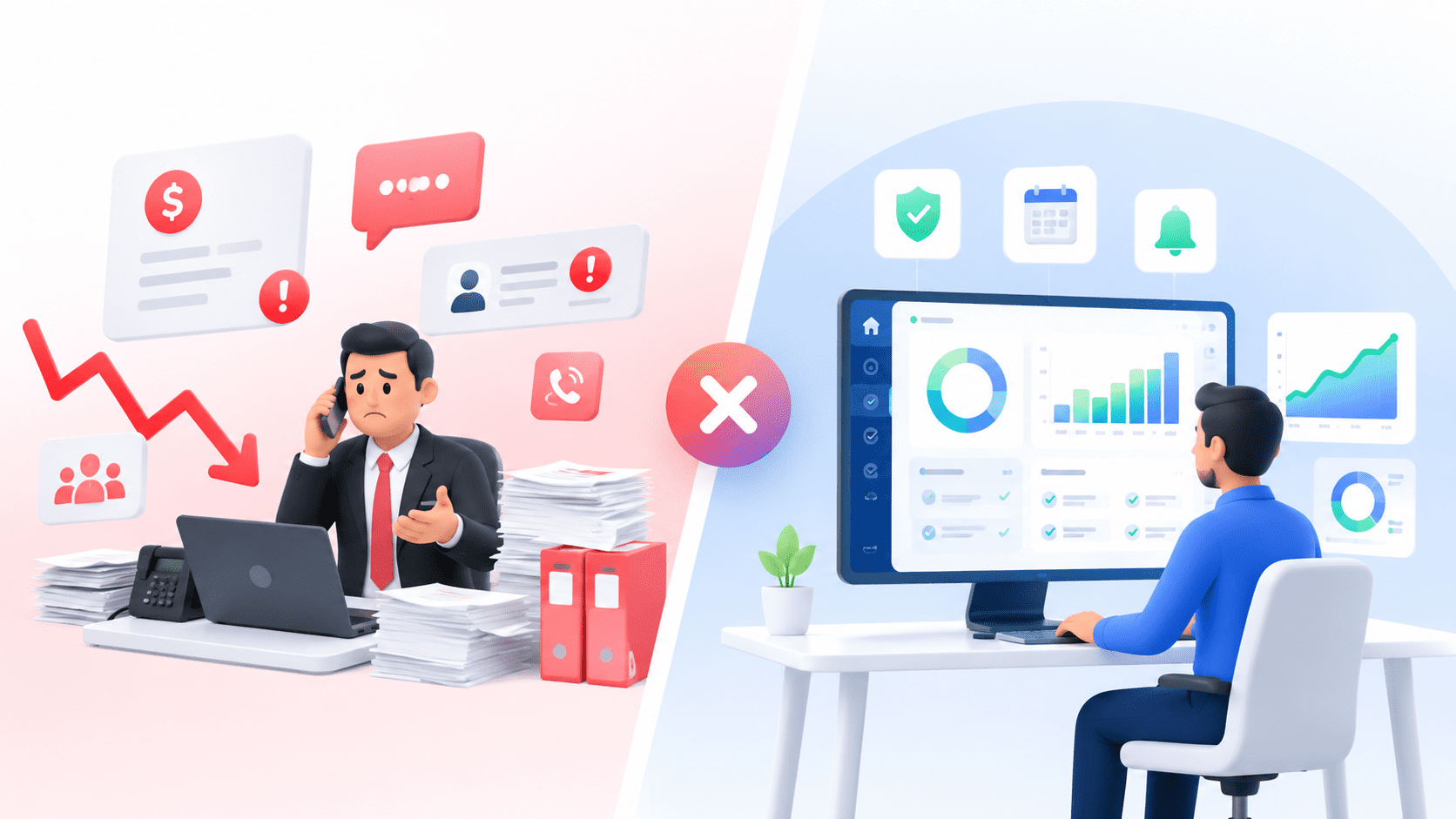

Collection Agencies Are Not The Best for Collections: Explained

When cash flow tightens, many businesses instinctively turn to collection agencies to recover overdue payments—but the reality is that a collection agencies are not the best for collections in today’s fast-moving, customer-first environment. What seems like a quick fix often results in higher costs, slower recovery, and a complete loss…

-

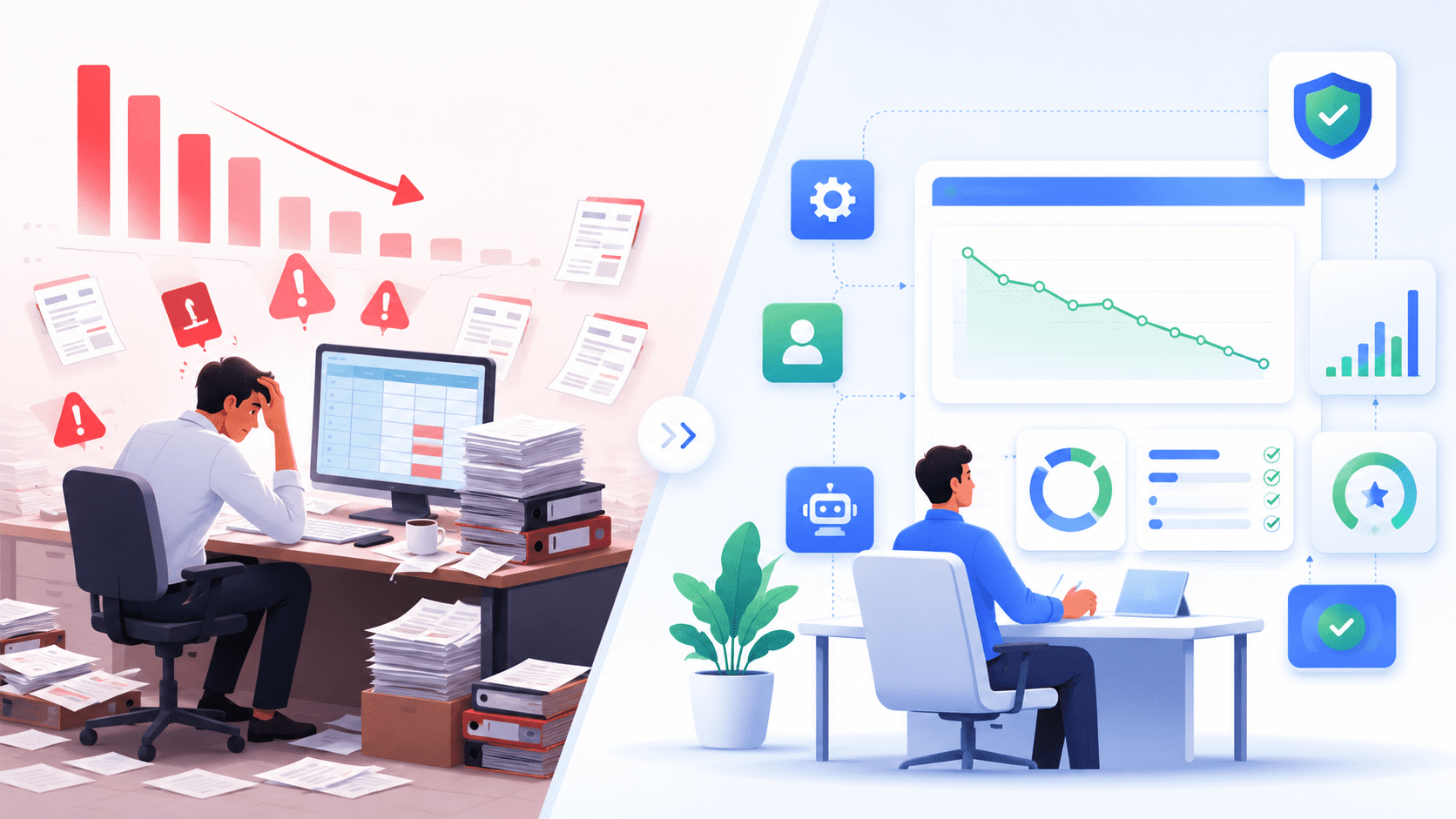

Debtor Days Explained: Formula + Proven Ways to Reduce It

If cash flow is the lifeblood of your business, then Debtor Days is your pulse check. Debtor Days (also known as Days Sales Outstanding or DSO) measures the average number of days it takes for a business to collect payment after a sale. The longer it takes, the more your…

-

Bad Debt Expense: Meaning, Formula & How to Reduce It

If you’re running a finance or AR function, Bad Debt Expense isn’t just an accounting term—it’s lost revenue, broken cash flow, and avoidable risk. In simple terms, Bad Debt Expense refers to the portion of receivables that your business does not expect to collect. But the real problem? Most companies…